DeFi Post-Crash: Why Investor Trends Don't Add Up (Rektrospective Realness)

DeFi's October Reckoning: Buybacks, Bargain Hunting, or Just a Bear Trap?

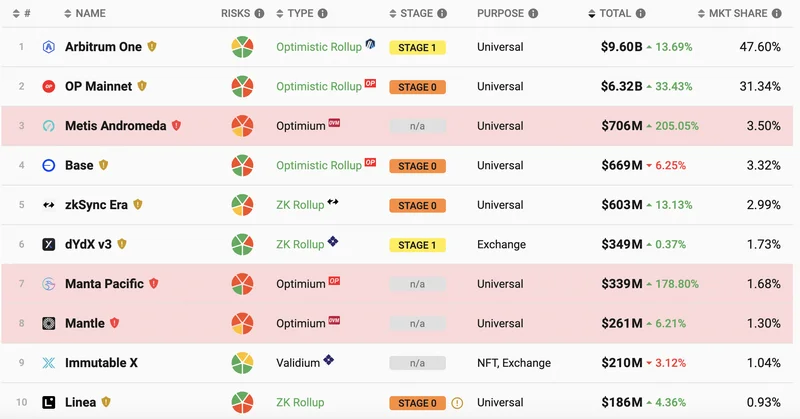

The October 10th crypto crash continues to cast a long shadow, especially over the decentralized finance (DeFi) sector. We're not just talking about a dip; we're talking about a potential paradigm shift. FalconX data shows that as of November 20, 2025, only two out of 23 leading DeFi tokens are in the green year-to-date. That's a sea of red, averaging a 37% drop quarter-to-date. But averages can be deceiving. Let's dig into what's really happening. For a deeper dive into the numbers and trends shaping the DeFi landscape after the crash, see "DeFi Token Performance & Investor Trends Post-October Crash."

The Great Rotation: Safety, Catalysts, and the Illusion of Value

Flight to Safety: Buybacks and Perceived Intrinsic Value

The initial reaction to the crash seems to have been a flight to perceived safety. Tokens with active buyback programs, like HYPE (down 16% QTD) and CAKE (down 12% QTD), have shown relative resilience. Investors, spooked by the broader market carnage, are clinging to anything that hints at intrinsic value or at least a floor on price declines. This isn’t exactly a ringing endorsement of the DeFi space; it’s more like rearranging deck chairs on the Titanic. The question is, are these buybacks actually effective, or just a temporary sugar rush funded by dwindling reserves?

Fundamental Catalysts: Navigating the Storm

Then there are the tokens buoyed by "fundamental catalysts," like MORPHO (down a mere 1% QTD) and SYRUP (down 13% QTD). These catalysts, such as minimal impact from the Stream finance collapse or unexpected growth spurts, suggest that some projects are navigating the storm better than others. But idiosyncratic success stories don't necessarily translate to sector-wide recovery. It's like celebrating a single tree that survived a forest fire.

Shifting Valuations: Price vs. Utility

The real head-scratcher is the shifting valuation landscape. While spot and perpetual decentralized exchanges (DEXs) have seen their price-to-sales multiples compress (price declining faster than protocol activity), some DEXs – CRV, RUNE, and CAKE, specifically – are posting greater 30-day fees as of November 20th compared to September 30th. This suggests that while investor sentiment is down, actual usage might be holding steady, or even increasing in certain niches. Are we seeing a genuine decoupling of price from utility, or is this a temporary blip before the next leg down?

Lending's Last Stand: The "Stickiness" Myth and the Search for Yield

The "Stickiness" Narrative: Lending in a Downturn

The lending sector presents an even more complex picture. Lending and yield names have generally seen their multiples steepen (price declining less than fees). KMNO, for example, saw its market cap fall 13% while fees declined a much steeper 34%. The prevailing narrative is that lending and yield activities are "stickier" than trading activities during a downturn. The logic? As investors flee to stablecoins, they'll seek yield opportunities to offset inflation.

Questioning the "Stickiness": Risks and Realities

But is this "stickiness" a real phenomenon, or just wishful thinking? It assumes that investors have both the capital and the risk appetite to continue lending in a volatile environment. It also ignores the potential for cascading liquidations if collateral values plummet. Lending activity might pick up as investors exit to stablecoins, but it's a precarious game of musical chairs.

Discrepancies in Lending Data: A Cause for Concern

And this is the part of the report that I find genuinely puzzling: if lending is supposedly "safer" in a downturn, why are lending platforms still seeing significant fee declines? Are the stated fees accurate, or are platforms inflating these figures to attract investors? The discrepancy between the narrative and the data is too large to ignore.

The Allure of New Crypto Coins: Speculation vs. Infrastructure

Furthermore, the surge of "new crypto coins to invest in December 2025," as Coinspeaker reports, adds another layer of complexity. Bitcoin Hyper (HYPER), Maxi Doge (MAXI), PEPENODE (PEPENODE), Ethena (ENA), and Remittix (RTX) are all vying for investor attention. HYPER, for instance, aims to be a Bitcoin Layer 2 solution with Solana-grade speed, boasting over 1.3 billion tokens staked in its presale. But with no public testnet, no public code, and anonymous developers, the 40% staking APY looks unsustainable. It's speculation on promises, not proven infrastructure.

Data Doesn't Lie, But It Can Be Misleading

The DeFi market is in a state of flux. Some sectors are showing signs of resilience, while others are struggling to stay afloat. Investors are flocking to perceived safety and chasing short-term catalysts, but the long-term outlook remains uncertain. The key takeaway? Don't be swayed by narratives or averages. Dig into the data, scrutinize the fundamentals, and always question the underlying assumptions. The market's "humility," as Andy Baehr notes, is welcome, but it shouldn't lull us into complacency.

The Price of "Stickiness"

The market is a complex beast. It's hard to say whether these trends mark the beginning of a broader shift in DeFi valuations or if they will revert over time. The only certainty is that volatility will continue to reign supreme. Approach with caution, and always do your own due diligence.

-

Warren Buffett's OXY Stock Play: The Latest Drama, Buffett's Angle, and Why You Shouldn't Believe the Hype

Solet'sgetthisstraight.Occide...

-

The Great Up-Leveling: What's Happening Now and How We Step Up

Haveyoueverfeltlikeyou'redri...

-

The Future of Auto Parts: How to Find Any Part Instantly and What Comes Next

Walkintoany`autoparts`store—a...

-

Applied Digital (APLD) Stock: Analyzing the Surge, Analyst Targets, and Its Real Valuation

AppliedDigital'sParabolicRise:...

-

Analyzing Robinhood: What the New Gold Card Means for its 2025 Stock Price

Robinhood's$123BillionBet:IsT...

- Search

- Recently Published

-

- Why Crypto Market Volatility is a Hidden Gift (r/Crypto)

- DeFi Post-Crash: Why Investor Trends Don't Add Up (Rektrospective Realness)

- Why Crypto's Recovery is a Lie. (- Hot Takes)

- Crypto's Future: Why Today's Challenges Spark Genius. (- Thread)

- Bitcoin's Volatility: Our Future Premium, Beyond VIX - Buckle Up, Buttercups!

- Tariffs Broke It. AI's Supposedly Fixing It. - Tech to the Rescue

- Crypto ETFs Tanked 80%: Retail Traders, You Got Played. - Ouch, Reddit!

- DeFi Token Performance Post-October Crash: what's really happening and who's left holding the bag

- Decentralized Finance: What it is, and why the 'decentralized' part is a joke.

- DeFi Token Performance & Investor Trends Post-October Crash: what they won't tell you about investors and the bleak 2025 ahead

- Tag list

-

- Blockchain (11)

- Decentralization (5)

- Smart Contracts (4)

- Cryptocurrency (26)

- DeFi (5)

- Bitcoin (31)

- Trump (5)

- Ethereum (8)

- Pudgy Penguins (6)

- NFT (5)

- Solana (5)

- cryptocurrency (6)

- bitcoin (7)

- Plasma (5)

- Zcash (12)

- Aster (10)

- nbis stock (5)

- iren stock (5)

- crypto (7)

- ZKsync (5)

- irs stimulus checks 2025 (6)

- pi (6)

- hims stock (4)

- kimberly clark (5)

- uae (5)